Credit and Debit Cards have made cashless payments the norm - whether you're shopping at a retail outlet or checking out online. They look identical, but they work very differently. Understanding those differences can help you choose the right card for the right situation.

What is a Credit Card and a Debit Card?

Credit Card

A Credit Card works on the principle of buying now and paying later. When you get one, the issuing bank assigns you a credit limit - the maximum you can spend on the card. Think of it as a short-term credit line you draw on for purchases. You can repay the borrowed amount in full or in instalments, by a predetermined due date. Pay in full and no interest is charged. Carry a balance forward, and interest applies to the unpaid amount.

Debit Card

A Debit Card is linked directly to your Savings or Current bank account. You can use it for online and offline payments, including ATM cash withdrawals. Every time you swipe or tap, the bank deducts the amount from your linked account in real time — you'll get an SMS with the transaction amount and your remaining balance right away.

Credit Card vs Debit Card: Comparing the features

Eligibility

Debit Cards are typically issued automatically when you open a bank account - no separate application needed. The card type depends on your account type and the balance you maintain. Credit Cards require a separate application: the issuer looks at your income, employment type, and credit history before approving one.

Nature of Usage

With a Credit Card, you borrow funds up to a pre-approved limit. The issuing bank pays the retailer on your behalf, then sends you a consolidated bill to repay by a fixed due date. With a Debit Card, funds come directly from your linked bank account — each transaction reduces your balance immediately.

Interest rate

Debit Cards involve no interest — you're spending your own money. Credit Cards charge interest on any outstanding balance not repaid in full by the due date. The rate varies by card and issuer — check your card's Most Important Terms and Conditions (MITC) for the applicable figure.

Spending limit

Credit Cards come with a pre-approved credit limit, set based on your income, repayment history, and credit profile — and it varies widely across individuals and card types. Debit Card spending is capped by what's in your bank account, with banks also applying daily and monthly transaction limits.

Rewards and privileges

Credit Cards typically offer a wider range of rewards - cashback, reward points, airmiles, airport lounge access, and exclusive deals on dining and travel. Debit Cards offer some rewards too, though the range is generally narrower. Premium Debit Cards from several banks have started closing that gap. Check what your card actually includes before writing it off.

Fees and charges

Both card types come with certain fees. Credit Cards may carry annual fees, late payment fees, cash advance fees, and foreign transaction fees — depending on the card. Debit Cards can attract charges for overdraft use, card re-issuance, international transactions, non-bank ATM withdrawals, and exceeding transaction limits.

Billing and Payments

With a Debit Card, there's no billing to manage — funds are deducted directly. With a Credit Card, two dates matter: the statement generation date and the payment due date. Pay your bill in full before the due date and you avoid interest entirely. Most card providers offer bill payment through their app or net banking portal.

ATM withdrawal

Both cards work at ATMs. With a Debit Card, you typically get a set number of free withdrawals each month — charges apply if you exceed the limit or use another bank's ATM. Withdrawing cash on a Credit Card attracts a cash advance fee and interest starts accruing from day one, with no grace period.

Security level

Both card types use two-step verification, SMS alerts, and CVV authentication. Credit Cards generally offer stronger fraud protection, many issuers cover zero or limited liability for unauthorised transactions, though the exact terms depend on your card's policy and how quickly you report the loss. Check with your issuer to know where you stand.

Credit Card vs Debit Card: Suitability

Think about your spending patterns

If you make frequent, smaller payments and want to stay within a fixed budget, a Debit Card is a simple option — you spend only what you have. A Credit Card works for both small and large purchases, giving you the flexibility to pay later and manage cash flow across billing cycles.

Evaluate your risk tolerance

Every Credit Card swipe is short-term debt — manageable if you repay on time, but costly if balances build up. A Debit Card carries no debt risk since you're always spending money already in your account.

Consider the benefits

Frequent travellers, diners, and online shoppers tend to get more value from Credit Cards — lounge access, restaurant offers, and shopping discounts can add up meaningfully. Debit Card benefits vary by bank and card type — some premium Debit Cards offer competitive perks, so review what yours includes before assuming there's nothing there.

Check if your credit score needs a boost

Responsible Credit Card usage — paying dues on time and in full — builds a healthy credit history, which matters when you apply for a loan down the line. Debit Card usage has no impact on your credit score either way.

Credit Card vs Debit Card: What Should You Choose

Both cards serve different purposes, and having both can work in your favour — use your Debit Card for everyday transactions and your Credit Card for larger purchases you'd like to spread across a billing cycle. The right choice depends on your spending habits, how disciplined you are with repayment, and the benefits you value most.

If travel is your priority, Scapia Co-branded Credit Cards are worth looking at — built for travellers who want to earn and redeem rewards without friction. With the Scapia Co-branded Credit Card , cardholders earn 10% rewards in the form of Scapia Coins on eligible domestic online and offline purchases made on Visa cards and 5% rewards in the form of Scapia Coins on eligible transactions made on RuPay cards. Cardholders can also enjoy 20% Scapia Coins back on travel bookings made on the Scapia app. Every 5 Scapia Coins convert to ₹1 — and there's no cap on how many you can accumulate. Cardholders can redeem instantly for flights, hotels, buses, trains, and more, directly through the Scapia app.

FAQs

Can I transfer money from my Credit Card to a bank account?

Yes. You can transfer via net banking, through a money transfer or e-wallet facility, or through your card's app. You can also withdraw cash at an ATM and deposit it elsewhere — but that route attracts a cash advance fee and immediate interest, so treat it as a last resort.

Which is better between a Debit Card and a Credit Card?

Neither is universally better — it depends on your needs. A Credit Card offers more rewards and flexibility if you repay consistently. A Debit Card is simpler and keeps you within your available balance, which makes it easier to stay out of debt.

How can I redeem rewards on a Credit Card?

It varies by card and issuer. Most providers let you redeem through their app or net banking portal — log in, go to the rewards section, and choose how to redeem. For Scapia Co-branded Credit Cards , cardholders can redeem Scapia Coins directly on the Scapia app for flights, hotels, buses, and trains.

How does the application process differ between a Debit Card and a Credit Card?

A Debit Card is usually issued automatically when you open a bank account — if not, you can apply online with basic details. A Credit Card requires a separate application: fill out a form with your personal and income details, and the issuer reviews your eligibility before approving and dispatching the card.

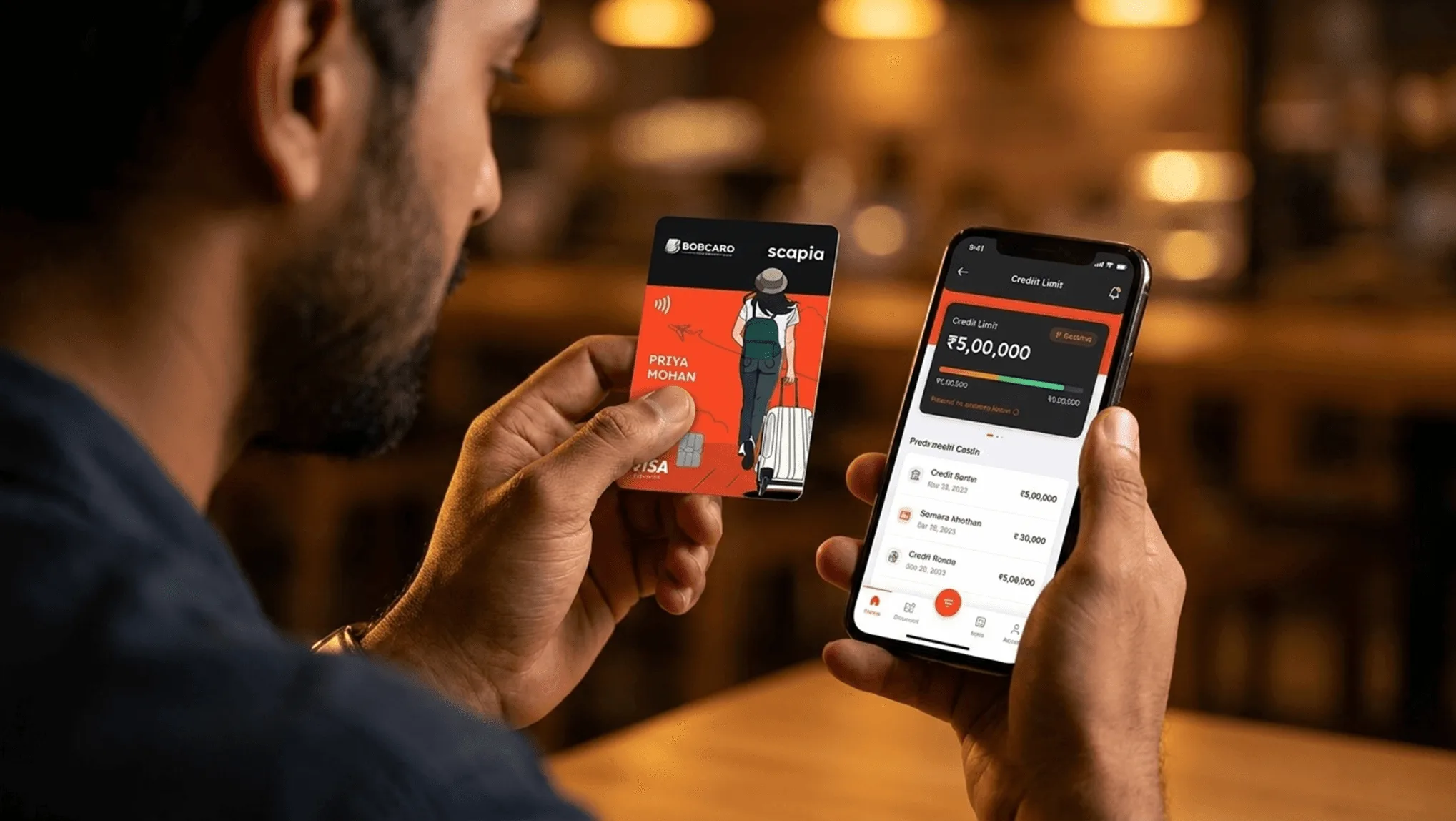

How is the credit limit on a Credit Card determined?

Issuers look at your net monthly income, credit score, employment history, and credit utilisation ratio. A strong income and a good credit history typically result in a higher limit.

What are the benefits of Debit and Credit Cards?

Debit Cards give you direct access to your funds and make spending easy to track via SMS alerts and mobile banking. Credit Cards let you buy now and pay later, earn rewards and cashback, and access exclusive services — the key is repaying on time to keep interest away.

What documents do I need to get a Debit Card and Credit Card?

For a Debit Card, standard account-opening documents apply — identity proof, address proof, PAN Card, and passport-sized photographs. For a Credit Card, you'll also need income proof like salary slips or IT returns, plus a completed application form and any additional documents the issuer asks for.