Your Credit Card is a financial tool, which solves your various payment-related concerns. Whether you want to buy a meal, purchase your favourite brands, or pay for utilities, you simply need to swipe your card, or tap it, or enter your PIN, and voila, your payment is done! Having a Credit Card proves helpful during emergencies or when you wish to purchase big-ticket items without having the funds debited from your Savings Account instantly. Knowing exactly how Credit Cards work is vital before applying for one.

Credit Cards – An Overview

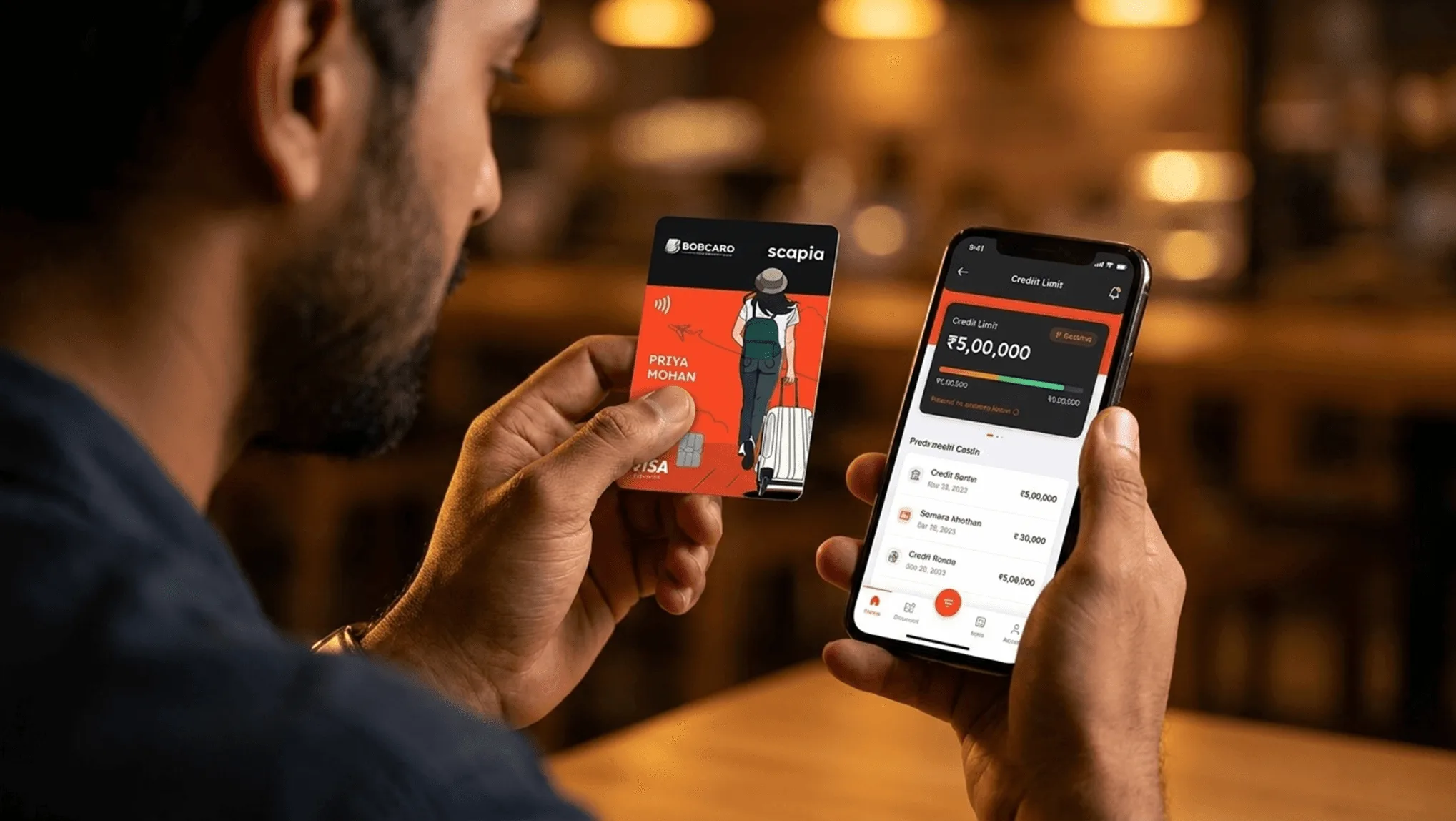

A Credit Card is a card you can use to pay bills, make purchases, or withdraw cash. Your card comes with a fixed credit limit, which the issuer determines based on your income and apparent creditworthiness. The credit limit reduces with usage and is replenished or reset on a fixed date, every month. If you keep using your card and paying off your dues on time, the issuer increases the credit limit frequently.

What Your Credit Card Looks Like – The Specifications

Your Credit Card includes the following details to enable unique, authentic transactions.

- The 16-digit card number

- The card validity and expiration date

- The name of the card holder

- The logo of the issuer, co-brand card partner and the network (Visa, MasterCard, Rupay, etc.)

- CVV number

- Contactless-enabled cards display a radio-wave symbol (four curved lines) on the card face

How do Credit Card payments work

The process of how Credit Cards work stays largely similar, whether you use the card online or at retail outlets. When you tap your Credit Card at a store or use it online the details of your card are sent to the retailer's bank. The Credit Card network then authorises the bank to process the transaction. Your card issuer approves or declines the transaction after verifying your information.

If the issuer approves the transaction, the payment is made to the merchant and your card's available credit limit gets deducted from the total limit. When your billing cycle ends, the card issuer sends you a statement showing all the transactions for that month, the new balance and your previous balance. The statement also comprises other vital details like, the minimum payment due and the due date.

If you repay your bill entirely on or before the due date, you are not charged any interest. But if you carry forward any balance amount from month to month, you will be charged interest by the issuer. Note that cash advances typically begin accruing interest from the date of withdrawal and do not benefit from an interest-free period.

Using Credit Cards Offline

After you have completed your purchase, present your Credit Card at the checkout counter. The storekeeper will insert your card into a point of sale (POS) machine to swipe it or simply tap the card on the machine, if the purchase amount is small. In most cases, you will have to authenticate the transaction by entering your Credit Card PIN.

The POS machine reads the chip or strip and sends the information along with the PIN to your issuing bank. If everything looks right (identity details, credit limit, validity, etc.) to the bank, the purchase is approved.

Once the purchase is approved, the POS machine prints a pair of receipts or charge slips – the merchant outlet keeps one and gives you the other copy. In case the PIN is not used you will be asked to sign the charge slip.

With this payment, the Credit Card issuer pays the merchant upfront on your behalf and bills you for the transaction in the next statement.

Using Credit Cards online

Let us now understand how Credit Cards work online. Once you have completed your purchases, and reach the check-out page, you can select Credit Card as the mode of payment. The system then prompts you to enter the following details to complete the purchase process:

- The 16-digit Credit Card number.

- The date of expiry on the card.

- The CVV printed on the flip side of the card.

- The name printed on the card.

After you enter these details and click on pay, the information goes to your bank via a payment gateway. You then receive an OTP from the bank on your email or mobile number to authenticate the transaction. Once you authenticate the transaction the purchase is completed.

Credit Card Fees

Some of the different types of fees associated with Credit Card payments include:

- Balance transfer fees: This fee is charged when you transfer the balance from another card, and is normally a percentage of the balance amount being transferred - the exact rate varies by issuer, so check your card's fee schedule.

- Over-limit fees: This fee is charged if your Credit Card spends exceed the prescribed credit limit set by the card issuer.

- Late fees: This fee is charged when you do not make the minimum payment by the due date.

- Annual fees: Some cards charge an annual or renewal fee for card membership, though many cards are available with zero joining and annual fees.

- Cash advance fees: Withdrawing cash using a Credit Card typically attracts a fee and higher interest from the date of withdrawal — check your card's terms for the applicable charges.

- Foreign transaction fees: Most cards levy a markup on international spends — the rate varies by issuer, so verify with your card provider before travelling abroad.

Different types of Credit Cards

You can divide Credit Cards into roughly two categories:

- Standard Credit Cards: These are the most basic cards which have limited features and no annual fees.

- Specialised Credit Cards: These are Credit Cards designed to cater to the specific needs of the cardholder. These cards come loaded with features and offers on shopping, dining, travel, etc.

Credit Cards can be further classified as:

- General Cards: Credit Cards which have basic features and zero or low annual fees. These cards are suitable for daily use.

- Reward Points Cards: These Credit Cards offer reward points to you on purchases that you make. The more you spend the more reward points you earn. These reward points can be redeemed against shopping vouchers from specific brands.

- Cash-back Credit Cards: These cards are different from reward point cards as they offer only cash in the form of cashback. A Cashback Credit Card will credit back a fixed or specific percentile amount to your account. The cashback is typically credited to your card account on a periodic basis - monthly or quarterly depending on the card - so check your card's terms for the exact redemption schedule.

Important Credit Card terms

Interest

Interest is an important term related to Credit Cards. When you swipe your Credit Card, you are essentially buying something by borrowing money on credit, also known as taking a loan. Just as you need to pay interest on loan, so do you need to pay interest on your Credit Card spends. However, the interest payments apply only when you do not pay your outstanding due applicable to a billing cycle. Essentially, the issuer charges interest only when you make partial payments of your Credit Card bills, and the interest is levied on the unpaid amount only. Credit card interest rates are expressed as an annual percentage rate (APR) and applied on a monthly basis to the outstanding balance. The exact rate varies by card and issuer — refer to your card's Most Important Terms & Conditions (MITC) for the applicable rate.

Credit limit

The maximum limit beyond which you cannot make any spends is known as the credit limit of your card. Any transactions done after the limit is spent will get rejected. Issuers determine your Credit limit based on various factors like your income and ability to pay, your credit score, the type of Credit Card you have, any other debts that you may have, and your record of timely payments. A good track record of paying your dues on time helps you get a higher credit limit.

Billing cycle

A billing cycle is the fixed timeline in which you can use your card until the next bill is raised. Spends done at the start of the cycle enjoy a longer interest-free credit period than spends done closer to the statement date.

Minimum payment

Credit Cards give you the facility to make a minimum payment every month instead of the whole amount. If you do not pay this amount, you are charged a fine. The amount over and above the minimum amount is carried forward but you need to pay interest on it.

Balance

The balance on your Credit Card statement is the amount you have used for spending but not yet paid back to the card issuer.

Why you should use a Credit Card

- Credit Cards offer great rewards and cashbacks which can help you get discounts on shopping, travel, dining, and more.

- Credit Cards can be a good way to keep a track of your spends and budget your finances accordingly. The monthly statements can work as good spend trackers.

- Credit Cards are also safer compared to cash, which, if stolen, is difficult to recover. If you lose your Credit Card, you can block it immediately and even dispute the unauthorised purchases.

- If used wisely - by paying dues on time and keeping your credit utilisation low - your Credit Card can help improve your credit score over time.

The best way to utilise your credit card rewards is to book flights and hotels, and enjoy the discounts and rewards offered with such transactions. This way, you can save a lot on your travel bookings and get access to the best rates. If you are a travel enthusiast, you should consider applying for the Scapia Federal Credit Card to unleash its travel benefits. Designed especially for travel lovers, this Credit Card generates savings and Scapia Coins with every booking. Cardholders can instantly redeem their Scapia Coins to book flights and hotels on the Scapia app. What's more, cardholders can use the card during overseas travels without incurring any forex markup fees.

FAQs

How to choose the right Credit Card?

The easiest way to select a suitable Credit Card is to compare various different cards offered by issuers. You should compare factors like the variable APR (annual percentage rate) for purchases, the promotional APR terms and conditions, the APR for balance transfers and cash advances, annual fees, rewards, etc.

What is Credit Card inactivity?

Credit Card inactivity is a term used to define the non-usage of a card for a long period of time. If you do not use your card for a specific duration as stated by the issuer, the issuer has the right to deactivate your card.

When can my Credit Card get deactivated?

There is no fixed timeline as to when your card can be deactivated. The deactivation policy varies for different issuers. Typically, issuers deactivate your card if there has been no activity on it for 6 or 12 consecutive months.

Per RBI guidelines, if you do not activate your new Credit Card within 30 days of issue, the card issuer must seek your OTP-based consent to activate it. If you do not provide consent, the issuer is required to close the card account within 7 working days of seeking that consent, without levying any charge.

What is the difference between a Debit Card and a Credit Card?

The main difference between the two cards is that you can use a Debit Card to directly withdraw money from your bank account. Conversely, when you swipe your Credit Card, the issuer pays the merchant on your behalf. This way, your Savings Account balances remain intact for the time being, until you repay your dues on or before the payment date.