You planned everything: the flights, hotels, and experiences. But somewhere between booking and landing, your credit card quietly added a charge on every foreign transaction. That's not a hidden charge. It's a forex markup, and it costs Indian travellers thousands on every trip. For frequent travellers, a forex travel card with no markup is a financial advantage. When you pair that with flights and hotel booking with rewards, and every trip starts paying you back.

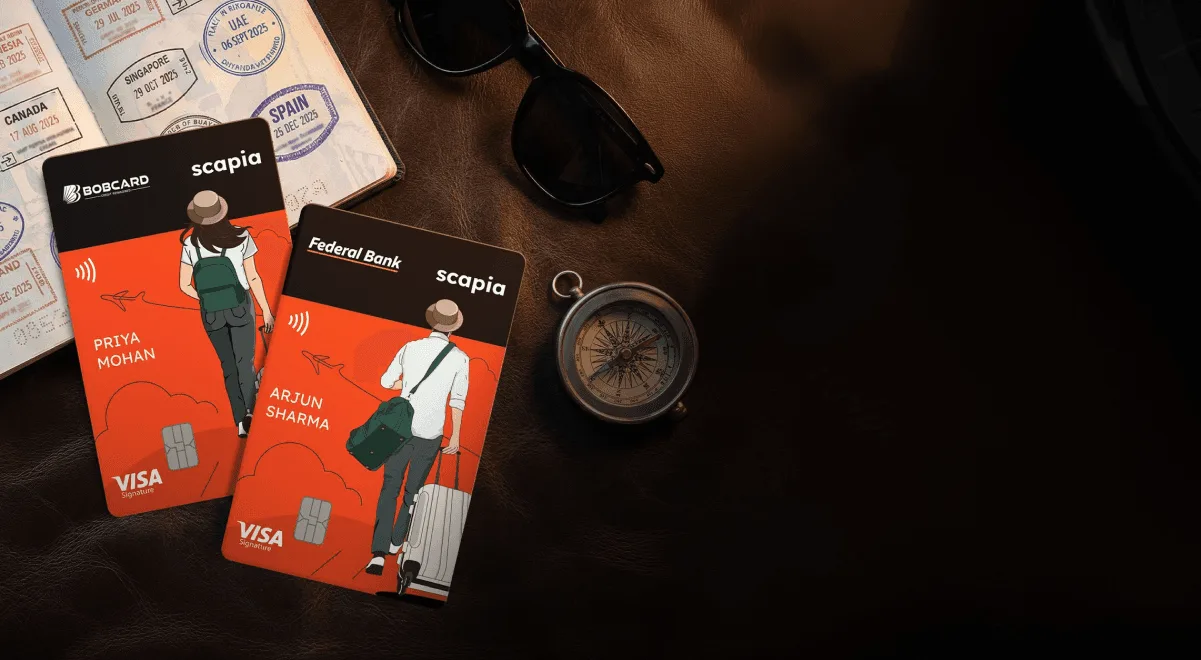

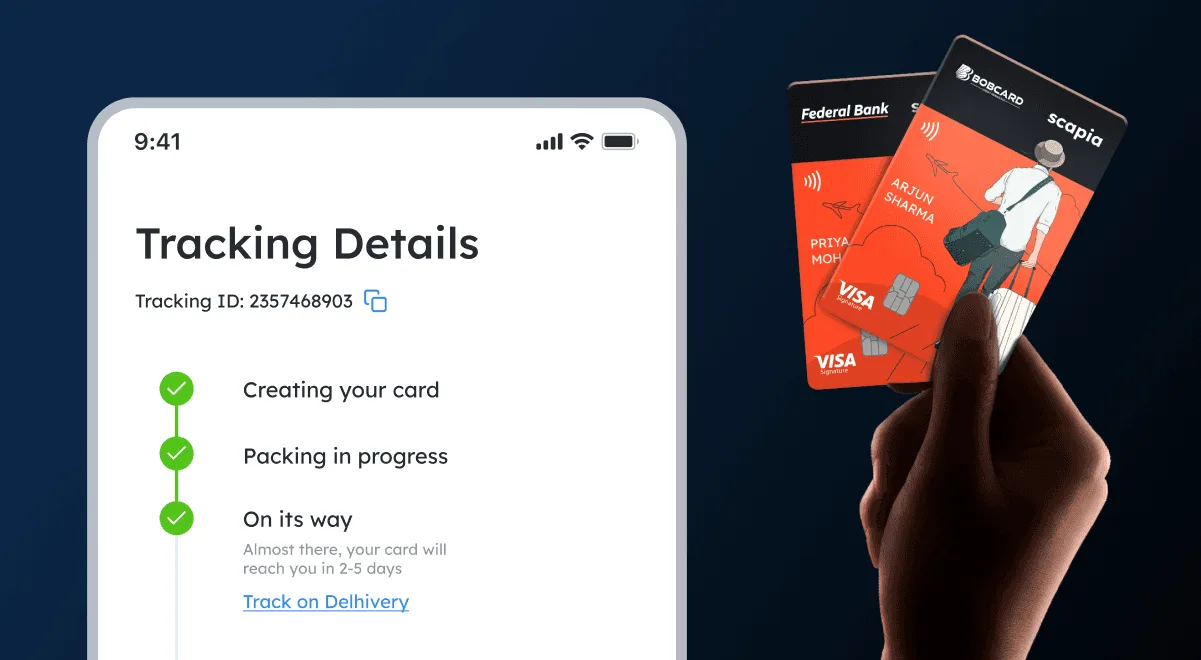

This guide walks you through how forex fees work, what to look for in an international travel card, and how the Scapia Co-branded Credit Card — issued in partnership with Federal Bank (Scapia Federal Credit Card) and BOBCARD (Scapia BOBCARD Credit Card) — is built for travel.

What Is A Forex Markup And Why Does It Matter?

When you make a payment in a foreign currency, your bank first converts it into INR using a network rate (typically set by Visa or Mastercard). Most banks then add a foreign currency markup — typically 2% to 3.5% — on top of that base rate. Some also layer in a GST of 18% on that markup.

These charges are part of how banks cover currency conversion and cross-border processing costs, but they can quietly increase your total spend. Along with other travel expenses like booking fees or dynamic pricing, it's one of the most overlooked costs for Indian travellers — and most reward credit cards don't waive it.

A zero forex fee credit card removes this extra charge entirely, so you pay only the converted amount, without markup or other hidden additions. For everyday expenses abroad - dining, shopping, local transport - the savings add up quickly over a trip.

The Difference Between Forex Cards And Credit Cards For Travel

Prepaid forex cards offer consistent conversion rates but come with their own limitations: reload hassles, limited currencies, and no rewards on spends. A credit card with zero forex markup gives you the best of both worlds: real-time conversion at the interbank rate, with the flexibility and rewards of a credit card.

What Should A Good International Travel Card Actually Do?

Not all travel credit cards are built equally. When evaluating one for international use, here's what actually matters:

- Zero forex markup: The baseline requirement. Anything above zero forex on a card used frequently abroad adds up.

- International spends: With zero forex markup, you can spend abroad without added currency conversion charges, so every foreign transaction costs you less.

- Flights and hotel booking with rewards: Travel bookings should earn meaningfully higher rewards, not just a marginal bump.

- Airport access: Lounge access before an international flight is a tangible benefit, especially for longer journeys or layovers.

- Zero to minimal annual fee: Premium travel cards often require ₹5,000 to ₹10,000 in annual fees to access forex-free benefits. A card with zero annual fees means you keep the benefit without paying for the privilege.

- Broad acceptance: Visa network coverage ensures the card works across 174+ countries without any compatibility issues.

How Does The Scapia Co-Branded Credit Card Handle International Travel?

The Scapia Co-branded Credit Card is built to keep travel - and the planning around it - simple and transparent. Here's how that plays out in practice.

Zero Forex Markup, no Conditions Attached

The Scapia Co-branded Credit Card charges zero forex markup on all international transactions. Spend internationally and pay the converted rate - nothing more.

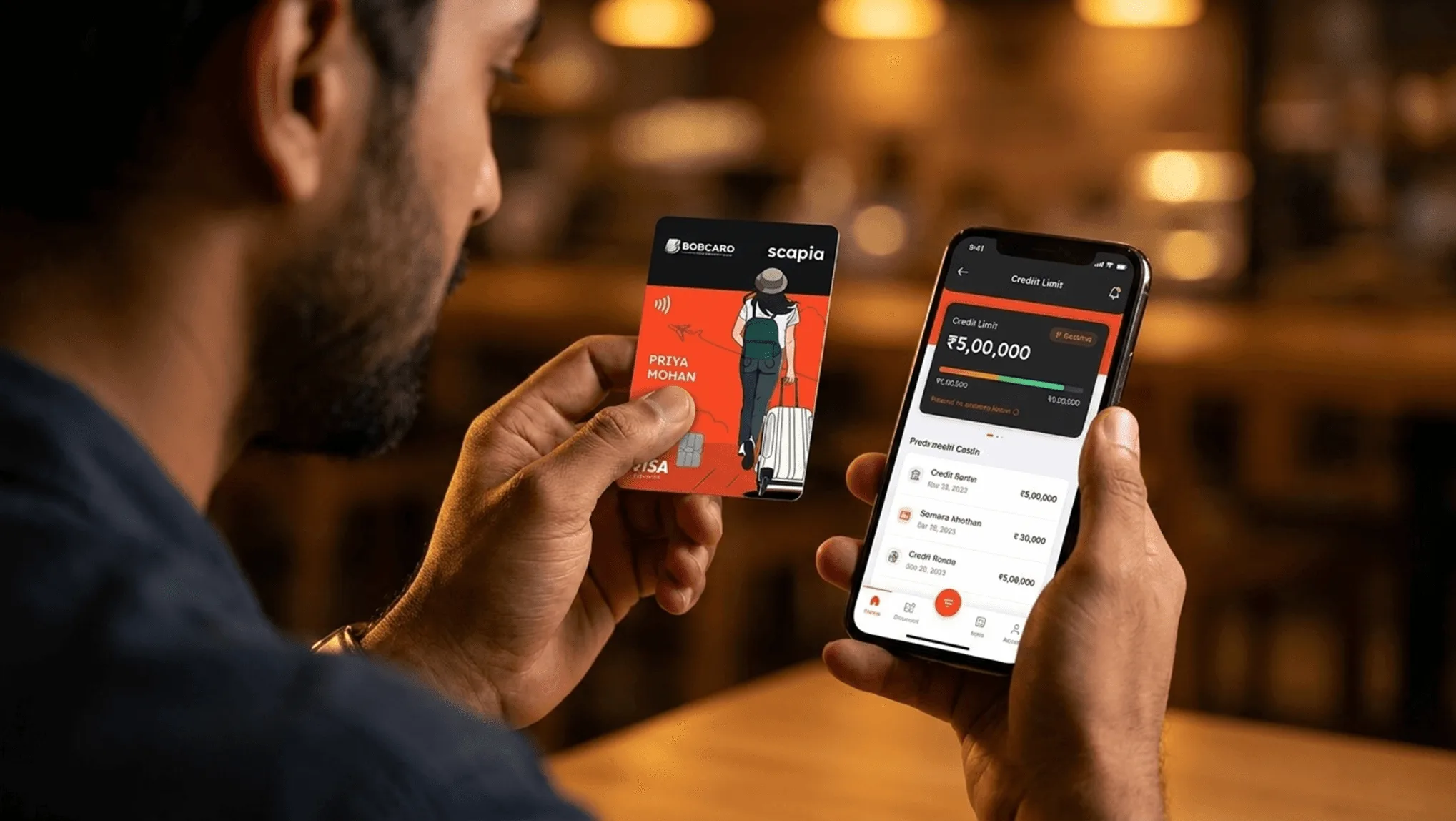

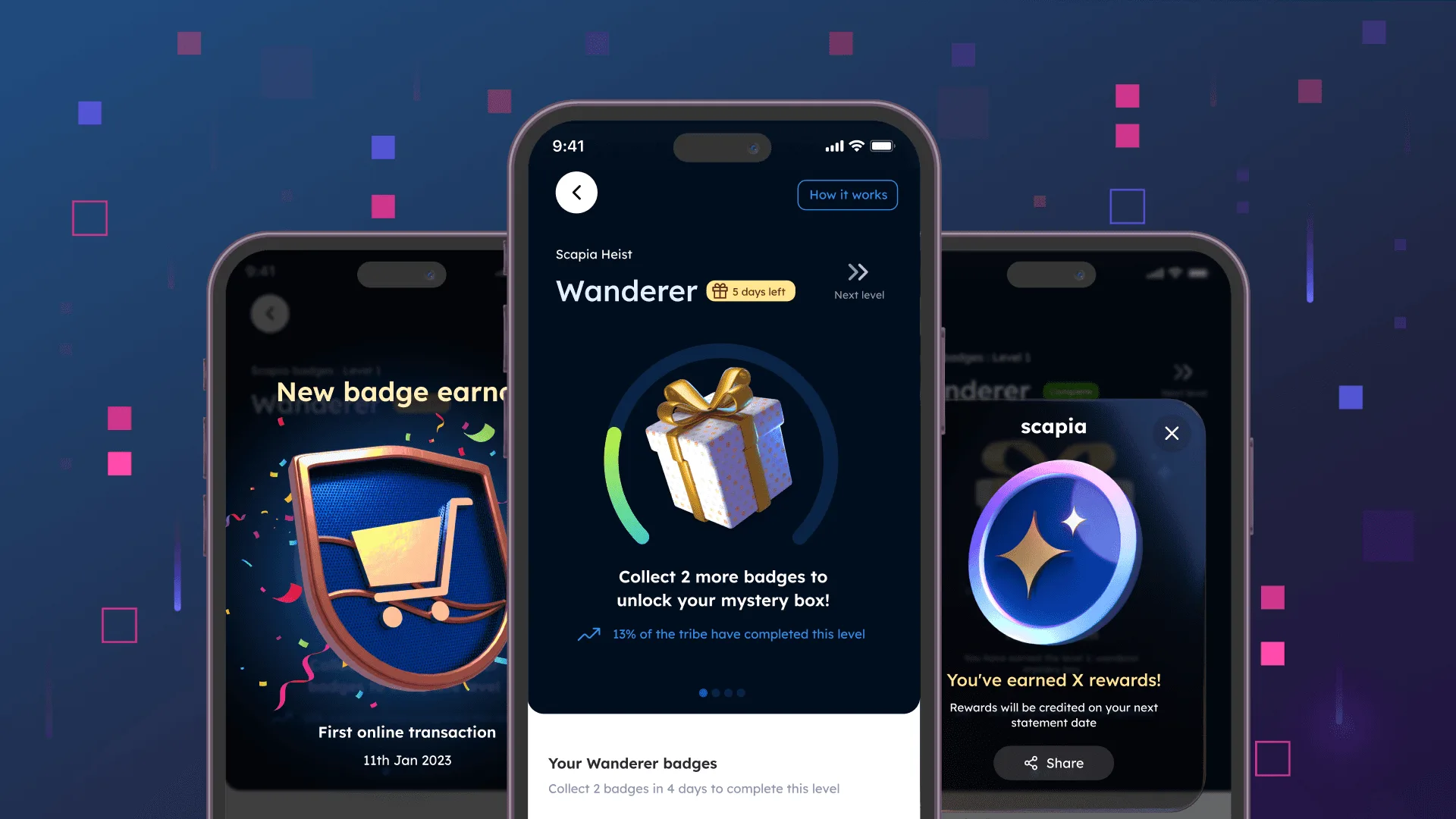

Earn Rewards You Can Actually Use

The card earns 10% Scapia Coins on Visa spends (minimum ₹20 per transaction), 5% on RuPay spends (minimum ₹500 per transaction), and 20% on travel bookings within the app. These coins convert at 5 coins = ₹1, redeemable directly on the Scapia app for flights, hotels, global travel experiences booking, visa applications, shopping, and more.

Zero Joining And Zero Annual Fees

The Scapia Co-branded Credit Card has zero joining fees and zero annual fees - whether you travel twice a year or twice a month.

Airport Privileges For Departures

The card covers both domestic and international airport privileges. Spend ₹20,000 or more in a month across your Visa and RuPay cards and get up to ₹1,000 back in Scapia Coins at domestic airport terminals. For international travel, book a flight of ₹50,000 or more through the Scapia app and receive ₹2,000 in Scapia Coins at international terminals.

A Travel Discovery Platform For Experiences

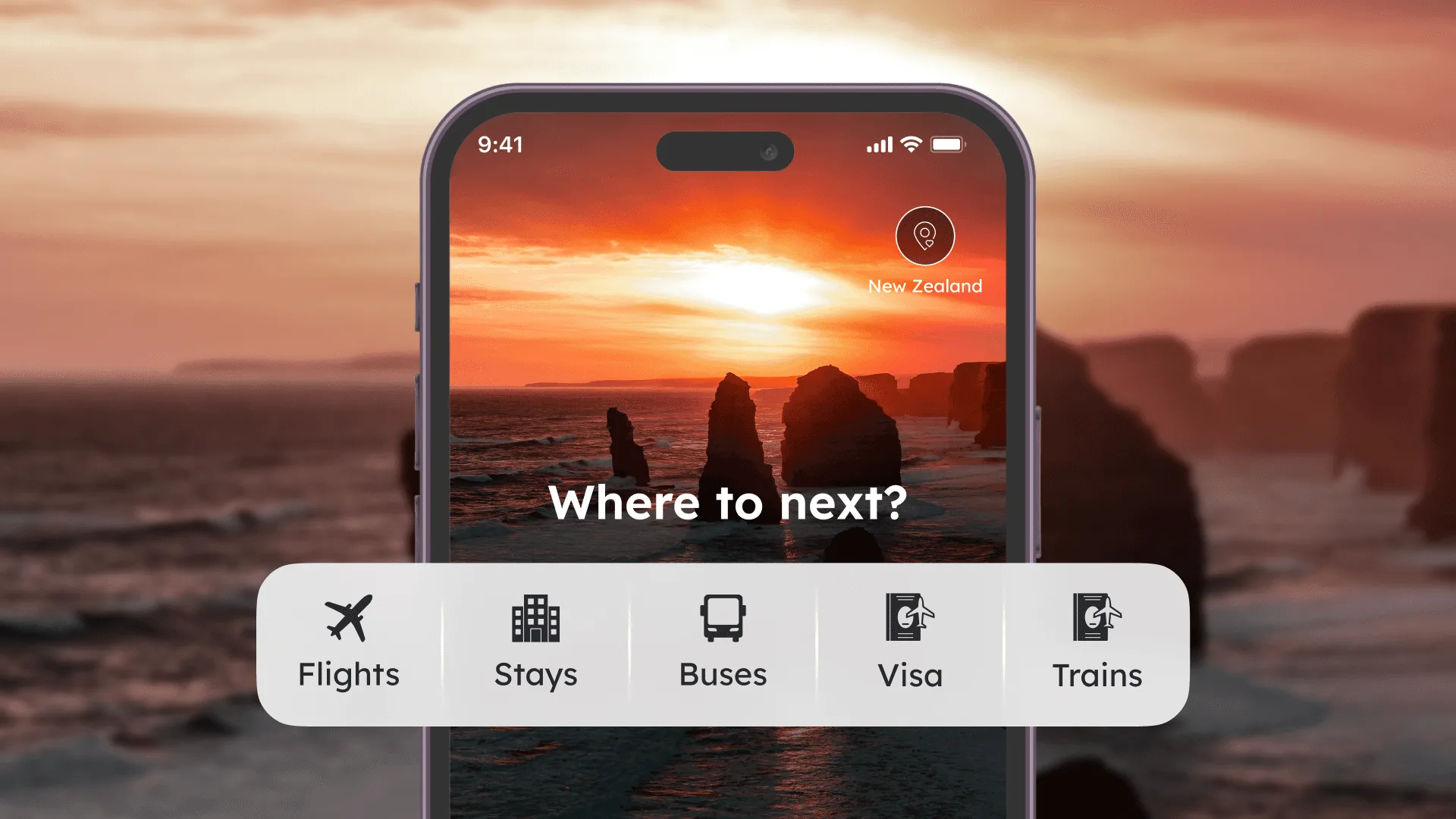

Beyond the card, the Scapia app brings together flights, 5 lakh+ hotels, trains, buses, visa assistance for 45 countries, and 22,000+ experiences worldwide. Cardholders also get access to Scapia Store (a curated selection of travel products) and Scapia Trips ( group journeys led by local experts built for travellers who want more than a standard tour). The Scapia app can also double as a travel discovery platform, helping cardholders discover stays, activities, accessories while planning a trip.

Smart Ways To Use Your Card Abroad

Here's how to get the most out of a zero forex fee credit card like Scapia Co-branded Credit Card when you’re an international trip:

- Book flights and hotels through the Scapia app before you travel to earn higher rewards, avail no-cost EMI options for international flights and stays.

- Use the Visa card for all foreign currency transactions like dining, shopping, and transport — without paying forex markup.

- Earn Scapia Coins on eligible domestic spends and redeem them when you book your next trip's flights or accommodation through the app.

- Skip the prepaid forex card entirely. The Scapia Co-branded Credit Card covers 170+ countries with no preloading.

Conclusion

International travel has enough moving parts without your credit card adding hidden costs at every turn. A forex travel card with no markup removes one of the most consistent — and most avoidable — drains on a travel budget. The Scapia Federal Credit Card and Scapia BOBCARD Credit Card handle that, while also earning you rewards on eligible spends and app bookings — backed by a travel platform that goes well beyond just card benefits.

FAQs:

What is a zero forex fee credit card, and how is it different from a regular travel card?

A zero forex fee credit card charges no foreign currency markup when you spend in a foreign currency. The Scapia Co-branded Credit Card waives this fee entirely, while regular credit cards typically add 2–3.5% on every foreign transaction.

Can I use the Scapia Co-Branded Credit Card in all countries?

Yes. The Scapia Co-branded Credit Card is accepted across 170+ countries on the Visa network. Cardholders have used it across 113 currencies globally.

Do I earn Scapia Coins on international spends?

No, Scapia Coins are not earned on forex transactions. You do get zero forex markup on international spends, which means no added conversion charge. For travel savings, use your card for eligible everyday spends to accumulate Scapia Coins, then redeem them on the Scapia app for flights, hotels, buses, trains, experiences, visa applications, Scapia Store, and Scapia Trips. Bookings and purchases made on the app earn 20% back in Scapia Coins.

Is the Scapia Co-Branded Credit Card free to use?

Yes. Scapia Co-branded Credit Cards come with zero joining fees and annual fees, with no hidden maintenance charges. Cardholders can also enjoy forex-free travel benefits, lounge access (subject to spend thresholds), and global travel experiences booking via the Scapia app are all included, no card fee required.

Planning an International Travel? Enjoy zero forex markup on your transactions abroad!

Get your Scapia Co-branded Credit Card!