A Credit Card's credit limit lets you make purchases - big and small - with ease. Staying on top of a few key Credit Card concepts can go a long way in making the most of your card. Knowing your billing date, statement date, outstanding bill amount, and unbilled amount gives you a clearer picture of your finances - and helps you avoid surprises when your next statement arrives.

Unbilled amount in Credit Card: Concept and example

The unbilled amount represents the part of your Credit Card expenses that haven't made it to your current month's Credit Card statement. These are usually transactions made after your Credit Card statement has been generated. You are required to pay for them in the next billing cycle — not the current one, for which a bill has already been generated and a due date set.

Say your Credit Card statement is generated on the 17th of each month, and your payment date is the 5th of every following month. Your statement covers all your transactions between the 17th of the previous month and the 16th of the current month. If you spend ₹2,00,000 during this billing cycle, you will need to pay this amount (partially or entirely) on or before the 5th of the next month (i.e.,your due date).

Any transactions you make on the 17th of the current month - the same day your statement is generated, or after - will show up as unbilled transactions and appear in the following month's statement.

Decoding how unbilled transactions in credit cards work

Once your Credit Card statement is generated, the amount shown is payable by the due date. There's typically a gap of 15 to 20 days between bill generation and the payment due date. Credit Card providers understand that you may need to make transactions during this period, so expenses incurred after the statement is generated are added to your next Credit Card statement as unbilled transactions.

To continue the example above: all expenses you incur after the bill is generated — from the 17th of the current month through to the 16th of the following month — will appear in the next month's statement.

The unbilled amount can be paid at any time - you don't have to wait for it to appear on your next statement. This gives you flexibility in managing your payments and helps you keep track of your overall credit utilisation. Amounts that remain unpaid are covered by the interest-free credit period — typically up to 55 days, depending on when in the billing cycle the spend was made. You can also convert high-ticket spends into EMIs - check your card's terms for the applicable window and conditions.

Ways to check your unbilled transactions in credit card

Card issuer's website or mobile app

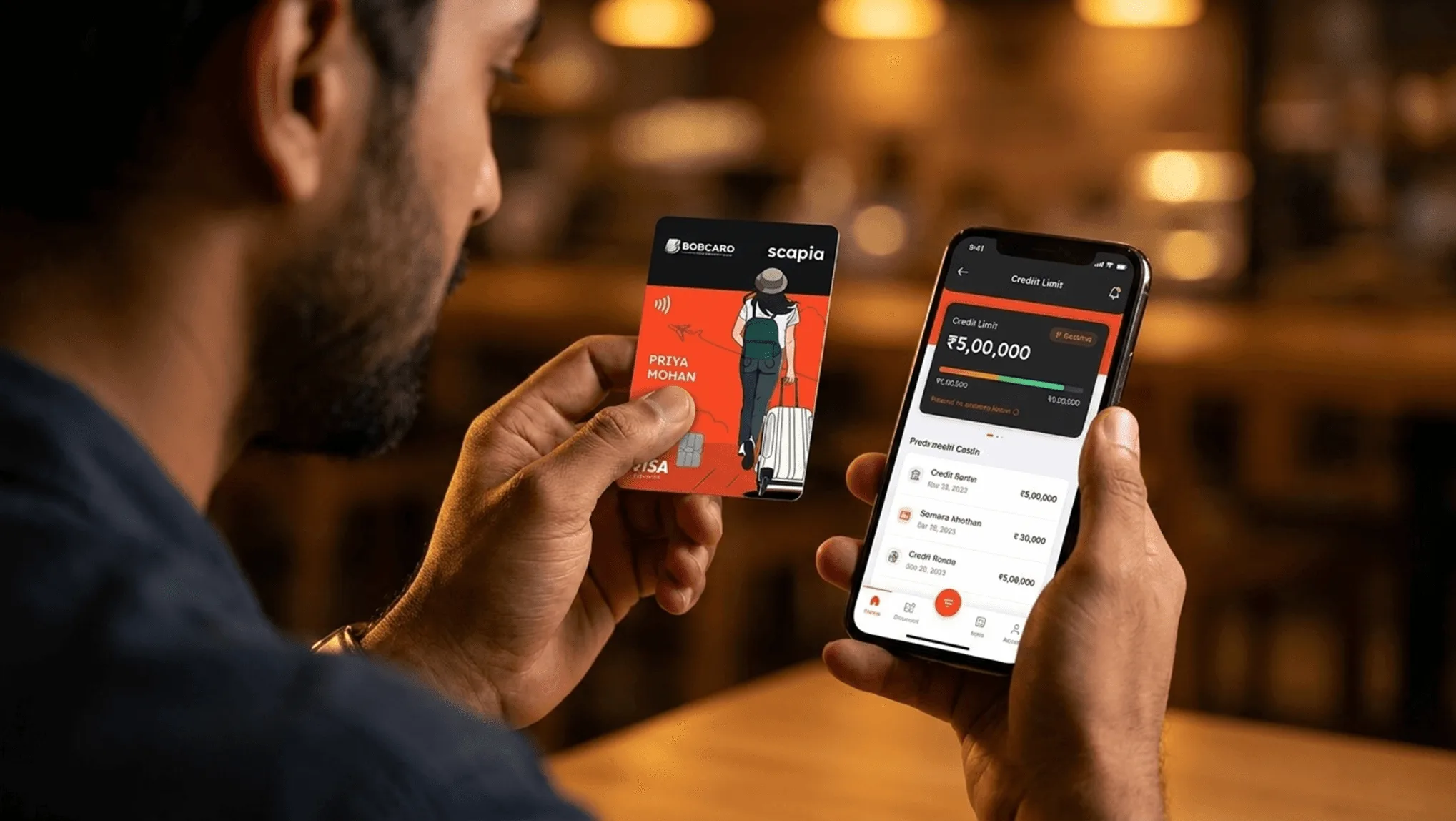

Most Credit Card providers offer a website or app where you can check your card information instantly. Log in and navigate to the card details or transactions section to view your unbilled transactions.

SMS notifications

Credit Card issuers send SMS notifications to your registered mobile number each time you use your card. Many also provide designated numbers where you can send an SMS to check your billing amount, unbilled transactions, and more.

Customer service helpline

Reach out to your card's customer care team to inquire about unbilled transactions, your available credit limit, and any other account details.

Types of unbilled transactions in a Credit Card

Your unbilled transactions could include:

- Online and offline purchases made after the Credit Card bill for the current billing cycle has been generated.

- Cash withdrawals made after the statement date.

- Pending or delayed processing charges — such as over-limit fees, late payment fees, or foreign transaction fees — for transactions made close to your billing date that have not yet been processed.

- Balance transfers initiated on your Credit Card to a bank account or another card.

- EMI instalments due after the statement date, for purchases previously converted to a repayment plan.

Check your unbilled Credit Card transactions effortlessly

Knowing your unbilled transactions gives you a clear view of your remaining credit limit and how much is coming up in your next bill — so there are no surprises when it arrives. The more visibility you have over your spending, the easier it is to stay on top of your finances.

FAQs

Is an unbilled Credit Card amount a point of concern?

Not necessarily. It's the part of your spending that hasn't yet appeared on your current statement — a normal part of card usage. That said, keeping an eye on your unbilled amount helps you stay within your credit limit and plan your upcoming payment.

Can I pay for unbilled transactions in Credit Card before the due date?

Yes. Unbilled transactions typically show up in your online account as pending or posted charges, and you can pay them off before they appear on your billing statement. You don't have to wait for the next statement — payment can be made alongside your current bill or at any other time that suits you.

Do unbilled transactions in Credit Card affect my credit score?

Unbilled transactions don't directly affect your credit score — credit bureaus consider the statement balance at the time of reporting. Paying your statement balance in full each cycle keeps your score healthy.

How is the unbilled amount in a Credit Card different from the statement balance?

The unbilled amount covers transactions made after the last billing cycle that haven't yet appeared on a statement. The statement balance is the total amount due at the end of a billing cycle — it includes billed transactions, applicable fees, and any outstanding balances carried forward.

Does the unbilled Credit Card amount accrue interest?

The unbilled amount doesn't accrue interest while it remains unbilled. Interest applies only after the amount appears on your statement and isn't paid in full by the due date. The one exception: cash withdrawals start accruing interest from the transaction date, regardless of the billing cycle. Always review your card's terms for the specific policy that applies.

Can I dispute any transactions included in the unbilled Credit Card amount?

Yes. If you notice any unauthorised usage, report it to your card's customer care team immediately. They'll guide you through the dispute process, investigate the transaction, and make sure you're not billed for something you didn't authorise. Be ready to provide supporting documentation if needed.

How can I manage and track the unbilled amount efficiently?

Keeping transaction records, setting up spending notifications, and reviewing your billing statement each cycle are all effective ways to stay on top of your unbilled amount. Most card providers also offer real-time tracking through their mobile app or net banking portal.